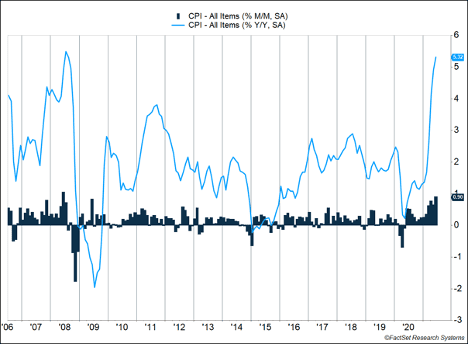

Two big economic releases in the U.S. and a series of economic data in China highlighted a challenging week for U.S. stocks. Inflation surged 0.9% and has now increased 5.4% over the last year (Figure 1). The U.S. Consumer Price Index increased more than expected, led by large spikes in used vehicle prices.

Key Points for the Week

- The Consumer Price Index surged 0.9% last month and is up 5.4% over the last year.

- S. retail sales added 0.6% aided by consumers buying more electronics, appliances, and clothing.

- China’s economy continues to rebound as industrial production rose 8.3% and retail sales rose 12.1% compared to last year.

Demand from retail consumers is likely contributing to price pressures. Retail increased 0.6% last month rather than falling 0.5% as economists expected. Some of the growth can be attributed to higher prices. Consumers seem to be sustaining the higher levels of spending that accompanied the most recent government stimulus. China’s economic recovery seems on surer footing. Industrial production rose 8.3% over the last year and retail sales rebounded 12.1% as China continues to grow in economic importance.

Stocks dropped last week in response to the economic data as well as concerns about how the Delta variant of COVID-19 will affect the economy. Last week, the S&P 500 shed 1.0%. Global stocks held up slightly better as the MSCI ACWI dipped 0.6%. The Bloomberg BarCap Aggregate Bond Index added 0.2%.

Economic releases will be fairly quiet this week. The Olympic opening ceremony is Friday as the games without fans begin. Earnings season continues as more of the S&P 500 reports.

Figure 1

Inflation is Moving Around

The U.S. Consumer Price Index rose 0.9% in June, which was 0.5% more than expected. The measure of U.S. consumer prices is up 5.4% over the last 12 months. It is rising faster than expected.

Food and energy prices increased more than normal. Food prices rose 0.8% and energy prices jumped 1.5%. Food and energy are generally more volatile than other areas of the economy, and many investors focus on core inflation, from which food and energy are excluded. Yet, that measure also leapt more than expected, rising 0.9% in June and climbing 4.5% over the last year.

What is causing the big moves in inflation? It turns out inflation is moving because more people are interested in moving around. Prices of items related to mobility are increasing faster than other items. The combination of used cars and trucks, new vehicles, car and truck rentals, lodging away from home, and airline fares accounted for 72% of the increase in core consumer prices.

Used car and truck prices have experienced the most rapid rise of the group, jumping 10.5% last month. The big increase follows hikes of 10% and 7.3% in the last two months. Over the last quarter, used car and truck prices have increased more than 30% and are up more than 45% over the last year.

Our view remains these seismic price changes in certain industries will slow in coming months. Automobile demand has increased significantly because of COVID-19. Public transportation and carpooling aren’t such attractive options during a pandemic, and people moving to less densely populated areas have few options, other than automobiles, to get around. New cars provide an alternative to used cars in most environments, but a shortage of microchips has slowed new car manufacturing and provided extra support for the used car market.

While sticking with our expectations for declining inflation, we are watching several factors closely to see if inflation trends are turning. Most international economies are also experiencing higher inflation but not to the same levels as the U.S. Job trends are another area of focus in our outlook. As enhanced unemployment benefits are set to expire, we’ll be watching if more unemployed workers are willing to return to jobs and relieve some of the pressure in industries experiencing a surge of demand.

If price increases don’t abate soon, they may force the Fed to move against inflation risk by cutting back on quantitative easing or signaling rates may rise sooner than expected. If that happens, it may have more market impact than higher inflation.

—

This newsletter was written and produced by CWM, LLC. Content in this material is for general information only and not intended to provide specific advice or recommendations for any individual. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. The views stated in this letter are not necessarily the opinion of any other named entity and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

S&P 500 INDEX

The Standard & Poor’s 500 Index is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

MSCI ACWI INDEX

The MSCI ACWI captures large- and mid-cap representation across 23 developed markets (DM) and 23 emerging markets (EM) countries*. With 2,480 constituents, the index covers approximately 85% of the global investable equity opportunity set.

Bloomberg U.S. Aggregate Bond Index

The Bloomberg U.S. Aggregate Bond Index is an index of the U.S. investment-grade fixed-rate bond market, including both government and corporate bonds.

https://www.statista.com/statistics/1034154/monthly-inflation-rates-developed-emerging-countries/

https://www.bls.gov/news.release/cpi.nr0.htm

https://www.cnbc.com/2021/07/16/us-retail-sales-unexpectedly-rise-0point6percent-in-june-.html

Compliance Case # 01084937